Evans Realty was established in 1985 and servicing the Treasure Valley for the past 39 years.

Homeowners Have Incredible Equity To Leverage Right Now

Even though home prices have moderated over the last year, many homeowners still have an incredible amount of equity. But what is equity? In the simplest terms, equity is the difference between the market value of your home and the amount you owe on your mortgage. The National Association of Realtors (NAR) explains how your equity grows over time:

“Housing wealth (home equity or net worth) gains are built up through price appreciation and by paying off the mortgage.”

How Your Equity Can Help You Achieve Your Goals

The equity you build up over the years can be used to your advantage when you sell your current house and buy your next home. If you no longer have the space you need, it might be time to move into a larger home. Or it’s possible you have too much space and need something smaller. No matter the situation, your equity can be a powerful tool you can use to help you make a move in today’s market. That’s because it may be some (if not all) of what you need for your down payment on your next home.

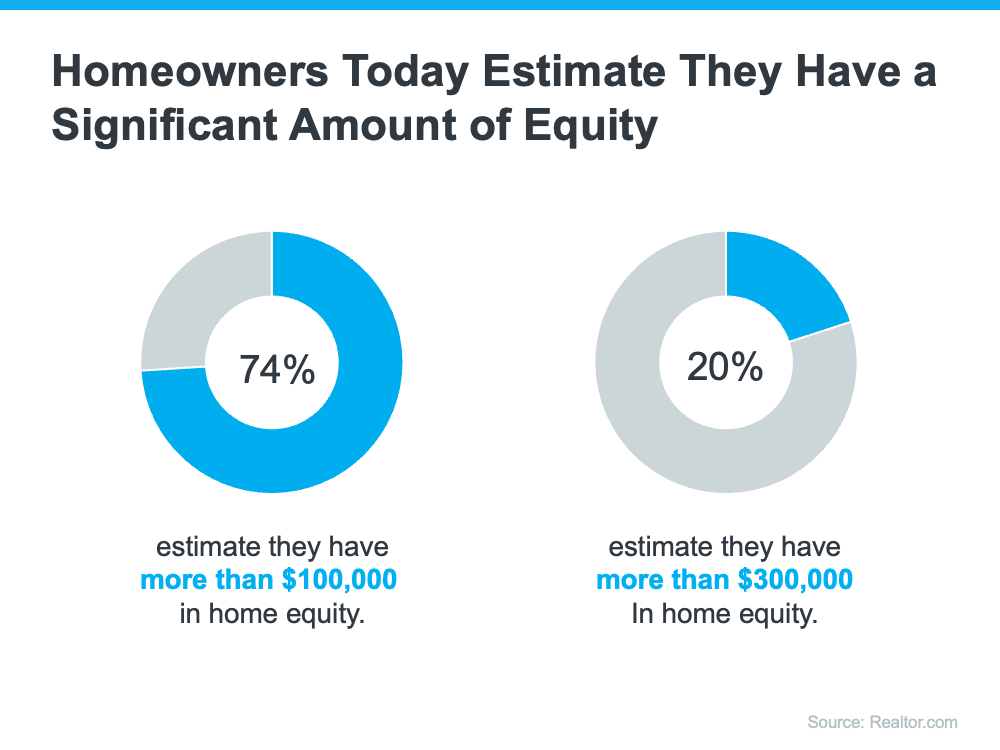

And how much equity you have may surprise you. A recent survey from Realtor.com finds many homeowners today estimate they’ve built up a significant amount of equity:

The latest data from CoreLogic helps solidify why homeowners are feeling so good about the equity they’ve likely gained over time. As Selma Hepp, Chief Economist for CoreLogic, says:

“While equity gains contracted in late 2022 due to home price declines in some regions, U.S. homeowners on average still have about $270,000 in equity, nearly $90,000 more than they had at the onset of the pandemic.”

How a Skilled Real Estate Agent Can Help

If you’re looking to leverage your equity to boost your buying power in today’s market, having a trusted agent by your side makes a difference.

A real estate professional can help you better understand the value of your home, so you’ll get a clearer picture of how much equity you likely have. As a recent article from Bankrate says:

“Hiring a skilled real estate agent can give you a realistic estimate of home prices in your area and how to price your current home. Using that figure, you can calculate how much equity you have and what your net proceeds will look like, so you can apply that money toward the down payment and closing costs of your new home.”

Having a solid understanding of your equity is key when it comes to making decisions about buying or selling your home. A skilled agent can help you navigate the often-complicated process of selling your house and ensure the transaction goes smoothly.

Bottom Line

Today, many homeowners are sitting on a substantial amount of equity, and you may be one of them. Let’s connect so we can estimate how much equity you have and plan how you can use it toward the purchase of your next home.

The Best Time To Sell Your House Is When Others Aren’t Selling

May 11, 2023

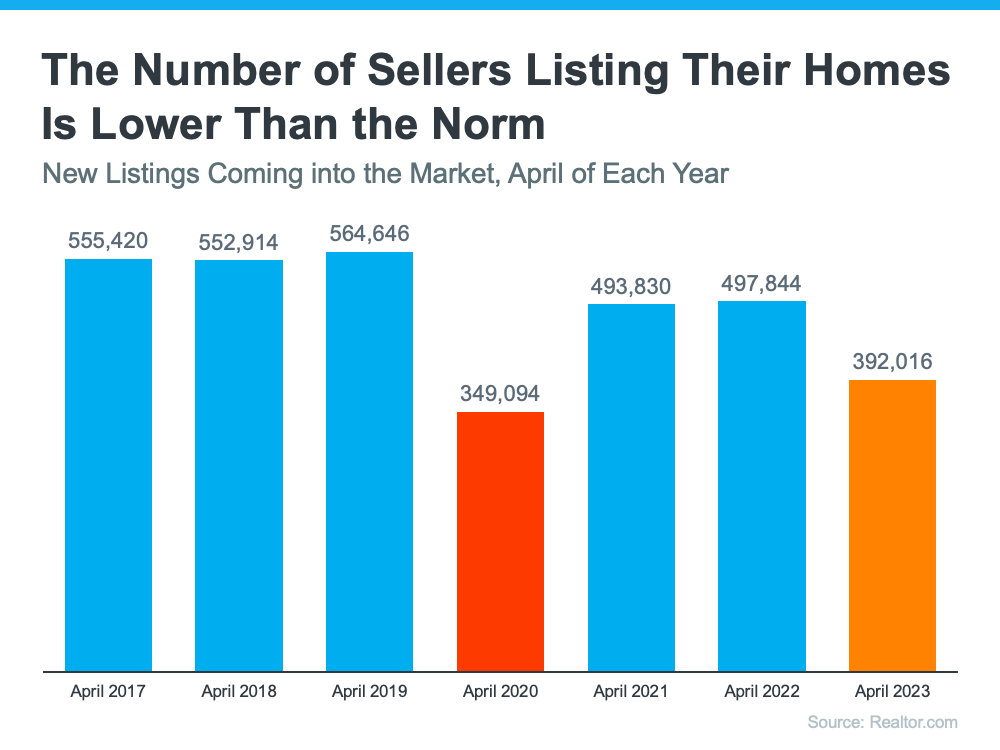

If you’re thinking about selling your house, you should know the number of homes for sale right now is low. That’s because, this season, there are fewer sellers listing their houses for sale than the norm.

Looking back at every April since 2017, the only year when fewer sellers listed their homes was in April 2020, when the pandemic hit and stalled the housing market (shown in red in the graph below). In more typical years, roughly 500,000 sellers add their homes to the market in April. This year, we saw fewer than 400,000 sellers entering the market in April (see graph below):

While there are a number of factors contributing to this trend, one thing keeping inventory low right now is that some homeowners are reluctant to move when the mortgage rate they have on their current house is lower than the one they could get today on their next house. It’s called rate lock.

As a recent survey from Realtor.com explains, 56% of people who are planning to sell in the next 12 months say they’re waiting for rates to come down.

While this wait-and-see approach is right for some sellers, it also creates an opening for more eager sellers to jump in now.

If your current house truly doesn’t fit your needs anymore and you’re ready to move, don’t miss this chance to stand out. When fewer sellers are putting their homes up for sale, buyers will have fewer options, so you set yourself up to get the most eyes possible on your house. That’s why your house could see multiple offers as buyers compete over the limited supply of homes for sale – especially if you price it right.

As Lawrence Yun, Chief Economist at the National Association of Realtors (NAR), says:

“Inventory levels are still at historic lows . . . Consequently, multiple offers are returning on a good number of properties."

Bottom Line

If you’re ready to sell now, beat the competition before it comes onto the market. If you do, your house should stand out and could get multiple offers. Let's connect to get you market ready.

The information contained, and the opinions expressed, in this article are not intended to be construed as investment advice. Keeping Current Matters, Inc. does not guarantee or warrant the accuracy or completeness of the information or opinions contained herein. Nothing herein should be construed as investment advice. You should always conduct your own research and due diligence and obtain professional advice before making any investment decision. Keeping Current Matters, Inc. will not be liable for any loss or damage caused by your reliance on the information or opinions contained herein.

The Impact of Inflation on Mortgage Rates

May 10, 2023

If you’re reading headlines about inflation or mortgage rates, you may see something about the recent decision from the Federal Reserve (the Fed). But what does it mean for you, the housing market, and your plans to buy a home? Here’s what you need to know.

Inflation and the Housing Market

While the Fed’s working hard to lower inflation, the latest data shows that, while the number has improved some, the inflation rate is still higher than the target (2%). That played a role in the Fed's decision to raise the Federal Funds Rate last week. As Bankrate explains:

“Keeping its inflation-fighting streak alive, the Federal Reserve has raised interest rates for the 10th time in 10 meetings . . . The hikes aimed to cool an economy that was on fire after rebounding from the coronavirus recession of 2020.”

While the Fed’s actions don’t directly dictate what happens with mortgage rates, their decisions do have an impact and contributed to the intentional cooldown in the housing market last year.

How This Impacts You

During times of high inflation, your everyday expenses go up. That means you’ve likely felt the pinch at the gas pump and in the grocery store. By raising the Federal Funds Rate, the Fed is actively trying to lower inflation. If the Fed is successful, it could also ultimately lead to lower mortgage rates and better homebuying affordability for you. That’s because when inflation is high, mortgage rates tend to be high. But, as inflation cools, experts say mortgage rates will likely fall.

Where Experts Think Mortgage Rates and Inflation Will Go from Here

Moving forward, both inflation and mortgage rates will continue to impact the housing market. And as Lawrence Yun, Chief Economist at the National Association of Realtors (NAR), says:

“Mortgage rates are likely to descend lower later in the year as the consumer price inflation calms down . . .”

Mike Fratantoni, Chief Economist at the Mortgage Bankers Association (MBA), explains:

“We continue to expect that mortgage rates will drift down over the course of the year as the economy slows . . .”

While there’s no way to say with certainty where mortgage rates will go from here, the experts think mortgage rates will trend down this year if inflation comes down too. To stay informed on the latest insights, connect with a trusted real estate advisor. They keep their pulse on what’s happening today and help you understand what the experts are projecting and how it could impact your homeownership plans.

Bottom Line

Don’t let headlines about the latest decision from the Fed confuse you. Where mortgage rates go from here depends on what happens with inflation. If inflation cools, mortgage rates should tick down as a result. Let’s connect so you have expert insights on housing market changes and what they mean for you.

The information contained, and the opinions expressed, in this article are not intended to be construed as investment advice. Keeping Current Matters, Inc. does not guarantee or warrant the accuracy or completeness of the information or opinions contained herein. Nothing herein should be construed as investment advice. You should always conduct your own research and due diligence and obtain professional advice before making any investment decision. Keeping Current Matters, Inc. will not be liable for any loss or damage caused by your reliance on the information or opinions contained herein.

Why Today’s Housing Market Is Not About To Crash

There’s been some concern lately that the housing market is headed for a crash. And given some of the affordability challenges in the housing market, along with a lot of recession talk in the media, it’s easy enough to understand why that worry has come up.

But the data clearly shows today’s market is very different than it was before the housing crash in 2008. Rest assured, this isn’t a repeat of what happened back then. Here’s why.

It’s Harder To Get a Loan Now

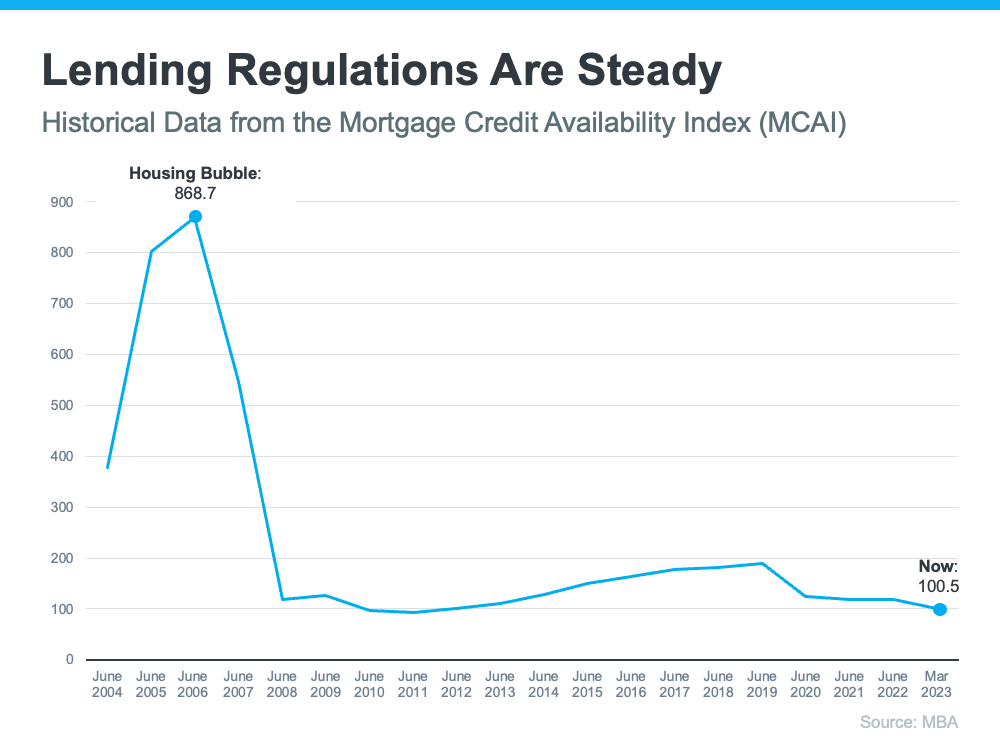

It was much easier to get a home loan during the lead-up to the 2008 housing crisis than it is today. Back then, banks had different lending standards, making it easy for just about anyone to qualify for a home loan or refinance an existing one. As a result, lending institutions took on much greater risk in both the person and the mortgage products offered. That led to mass defaults, foreclosures, and falling prices.

Things are different today as purchasers face increasingly higher standards from mortgage companies. The graph below uses data from the Mortgage Bankers Association (MBA) to show this difference. The lower the number, the harder it is to get a mortgage. The higher the number, the easier it is.

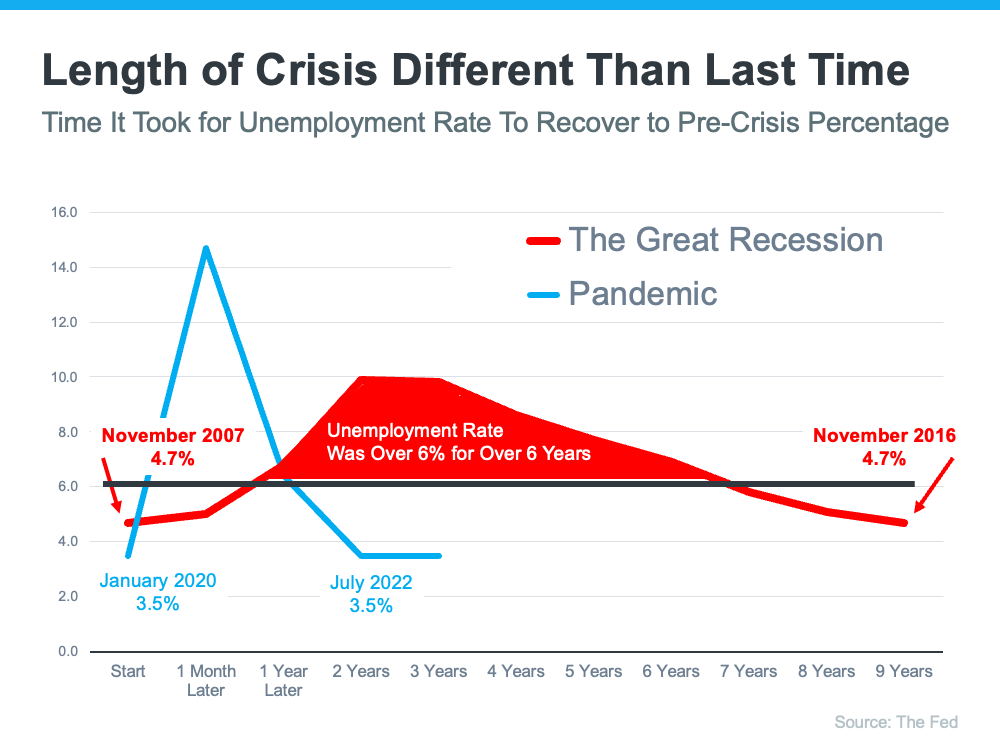

Unemployment Recovered Faster This Time

Unemployment Recovered Faster This Time

While the pandemic caused unemployment to spike over the last couple of years, the jobless rate has already recovered back to pre-pandemic levels (see the blue line in the graph below). Things were different during the Great Recession as a large number of people stayed unemployed for a much longer period of time (see the red in the graph below):

Here’s how the quick job recovery this time helps the housing market. Because so many people are employed today, there’s less risk of homeowners facing hardship and defaulting on their loans. This helps put today’s housing market on stronger footing and reduces the risk of more foreclosures coming onto the market.

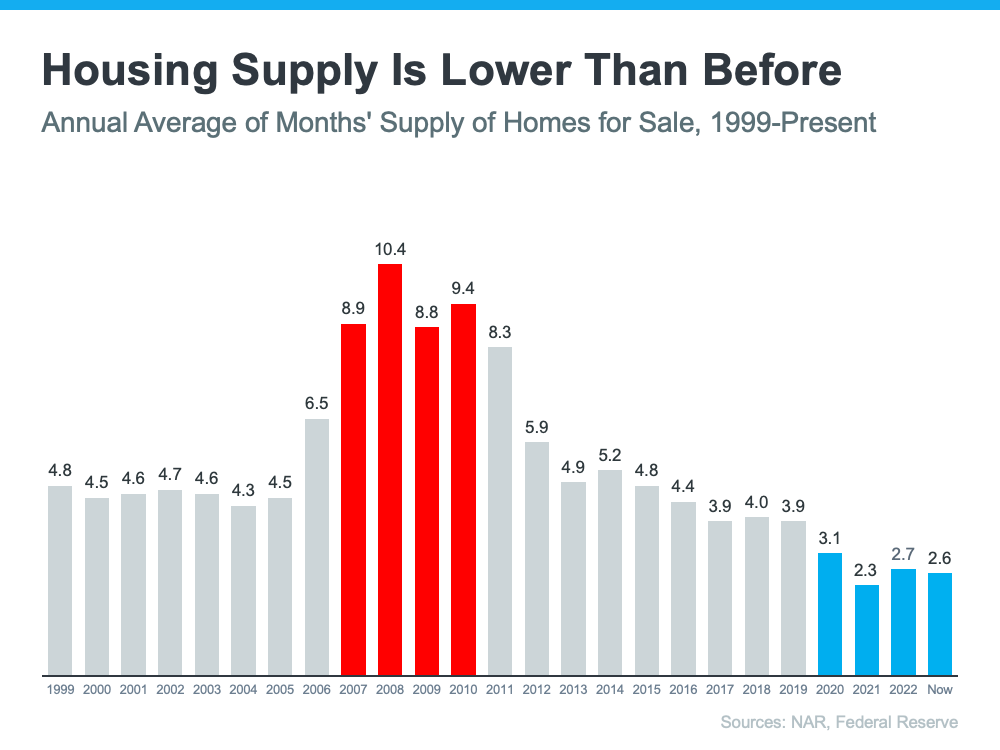

There Are Far Fewer Homes for Sale Today

There were also too many homes for sale during the housing crisis (many of which were short sales and foreclosures), and that caused prices to fall dramatically. Today, there’s a shortage of inventory available overall, primarily due to years of underbuilding homes.

The graph below uses data from the National Association of Realtors (NAR) and the Federal Reserve to show how the months’ supply of homes available now compares to the crash. Today, unsold inventory sits at just a 2.6-months’ supply. There just isn’t enough inventory on the market for home prices to come crashing down like they did in 2008.

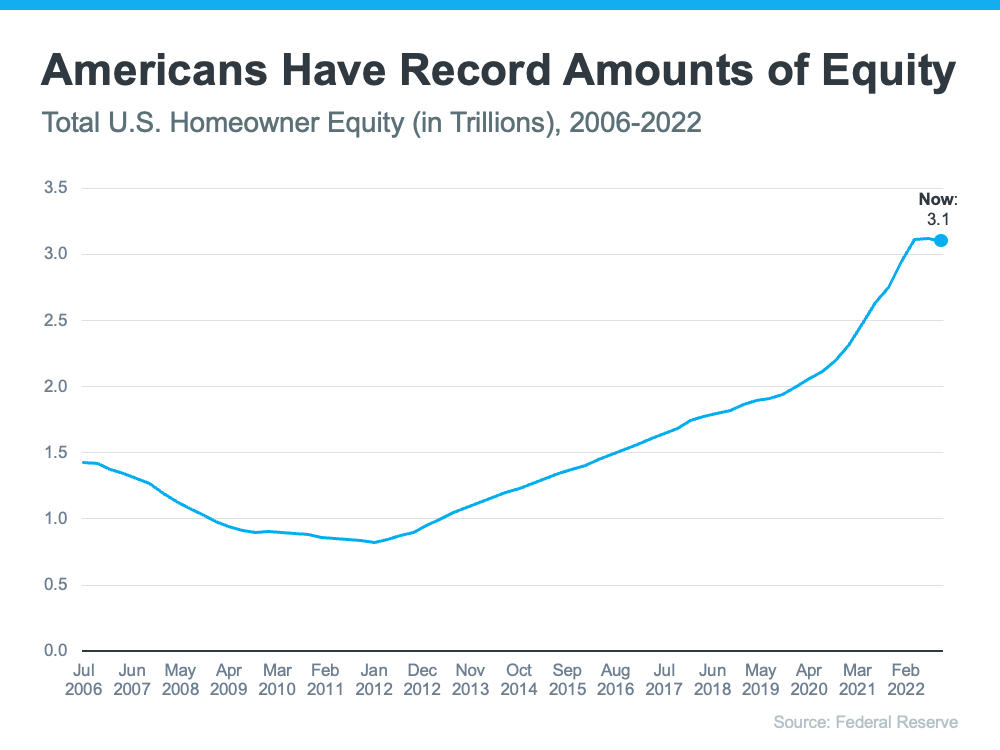

Equity Levels Are Near Record Highs

That low inventory of homes for sale helped keep upward pressure on home prices over the course of the pandemic. As a result, homeowners today have near-record amounts of equity (see graph below):

And, that equity puts them in a much stronger position compared to the Great Recession. Molly Boesel, Principal Economist at CoreLogic, explains:

“Most homeowners are well positioned to weather a shallow recession. More than a decade of home price increases has given homeowners record amounts of equity, which protects them from foreclosure should they fall behind on their mortgage payments.”

Bottom Line

The graphs above should ease any fears you may have that today’s housing market is headed for a crash. The most current data clearly shows that today’s market is nothing like it was last time.

It May Be Time To Consider a Newly Built Home

If you’re looking to buy a house, you may find today’s limited supply of homes available for sale challenging. When housing inventory is as low as it is right now, it can feel like a bit of an uphill battle to find the perfect home for you because there just isn’t that much to choose from. If you need to open up your pool of options, it may be time to consider a newly built home.

According to the latest data from the U.S. Census, there’s positive news when it comes to new home construction. When you look at the first three months of this year, you’ll find:

- More new homes were completed and are ready to sell. This gives you more move-in-ready options for your search.

- Builders broke ground and started construction on more single-family homes. This means there are more homes intended for one household in the beginning stages of construction, allowing you the opportunity to customize one to your liking.

- The number of permits for building new single-family homes ticked up. This shows builders are ramping up to start on even more home construction soon.

And, while this is all good news for broadening your options for your home search, there are other perks that come with considering a newly built home.

Customization

When you buy a new home under construction, you can tailor it to your unique needs and taste. Bankrate?says:

“Building means customizing. . . . instead of wishing your home had a certain kind of flooring, a sunroom or some other special amenity, you’ll be able to tailor the property to your exact needs.”

Brand New Everything

Another perk of a new home is that nothing in the house is used. It’s all brand new and uniquely yours from day one.

Minimal Repairs

And, because everything is new, you’ll likely find there are fewer maintenance and repair needs up front. As Realtor.com explains:

“. . . if something does go wrong with your new home, not only are there likely some manufacturer warranties in place, but many builders also include additional home warranties . . .”

Energy Efficiency

Lastly, building a home gives you the opportunity to incorporate more energy-efficient options that can help lower your costs over time – which can feel especially important when inflation’s raising many of the costs around you.

Bottom Line

If you’re having trouble finding your dream home in today’s market, it may be time to consider newly built homes as an option. Let’s connect so you have an expert on your side to help you explore what’s available in our local area.

|

Press Ctrl + D to bookmark this page

Web Accessibility Help Visually Impaired

Physical Difficulty

Audio Impaired

|

Member Agents | Privacy Policy

Realtor Websites by TourRE