Evans Realty was established in 1985 and servicing the Treasure Valley for the past 39 years.

Home Prices Are Climbing in These Top Cities

Thinking about buying a home or selling your current one to find a better fit? If so, you might be wondering what's going on with home prices these days. Here's the scoop.

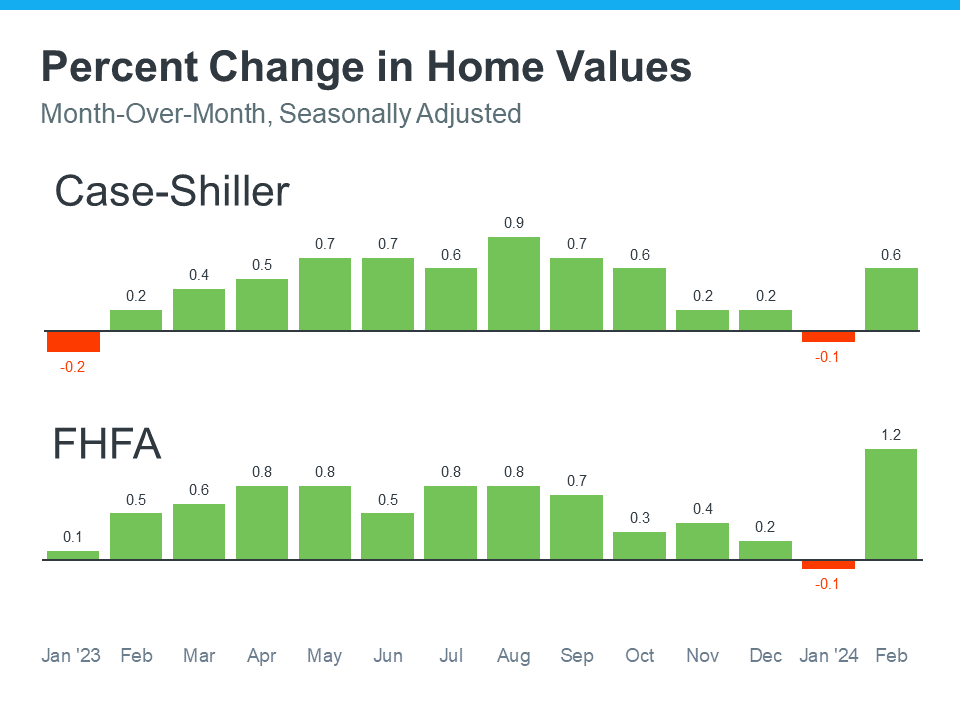

The latest national data from Case-Shiller and the Federal Housing Finance Agency (FHFA) shows they’re going up (see graphs below):

As you can see, home prices were rising for most of 2023. But over the course of December and January, they were virtually flat – which is pretty normal for that time of year.

But here's what you need to know now. As of February, when the spring market kicked off, prices were on the rise again.

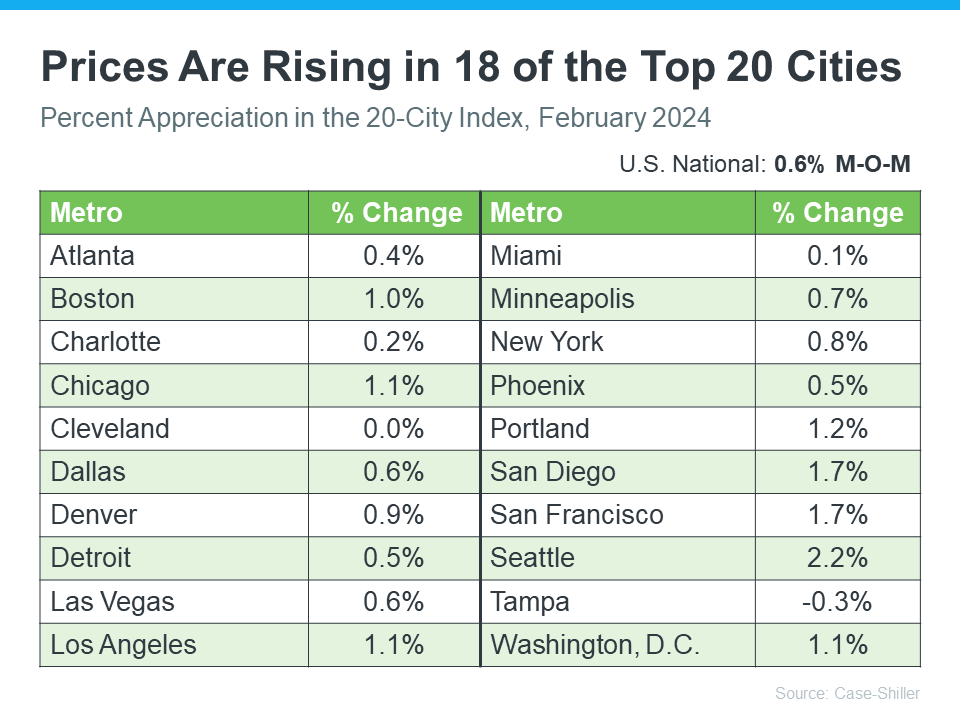

Home Prices Are Going Up in Most of America's Top Cities

After seeing a jump in home prices nationally in February, you might be wondering if they’re going up in your area, too. While it depends on where you live, prices are rising in 18 of the top 20 cities Case-Shiller reports on in the monthly price index (see chart below):

Most experts also think home prices will keep rising and end the year on a high note. Forbes explains why:

“Even as mortgage rates have reached their highest level since November, persistent demand coupled with limited housing supply are key drivers pushing home values upward.”

How This Impacts You

- For Buyers: If you’re ready, willing, and able to buy a home, purchasing before prices go up even more might be a smart choice, since home values are expected to keep climbing.

- For Sellers: Prices are going up because there still aren’t enough homes available for sale right now compared to today’s buyer demand. So, if you work with an agent to price your house right, you might receive multiple offers and sell quickly.

Bottom Line

The data shows home prices are increasing nationally. Let's chat to see exactly what’s going on with prices in our neighborhood.

The Top 2 Reasons To Consider a Newly Built Home

When you’re planning a move, it’s normal to wonder where you’ll end up and what your future home is going to look like. Maybe you’ve got a specific picture of that house in your mind. But unless you came into this process knowing you want to buy a newly built home, you may not have pictured new home construction.

A trusted real estate agent can help walk you through these two reasons you may want to reconsider that.

1. Adding Newly Built Homes Could Give You More Options

There are two types of homes on the market: new and existing. A newly built home refers to a house that was just built or is under construction. An existing home is one a previous homeowner has already lived in. Right now, the inventory of existing homes is tight. But there may be options for you on the new home side of things.

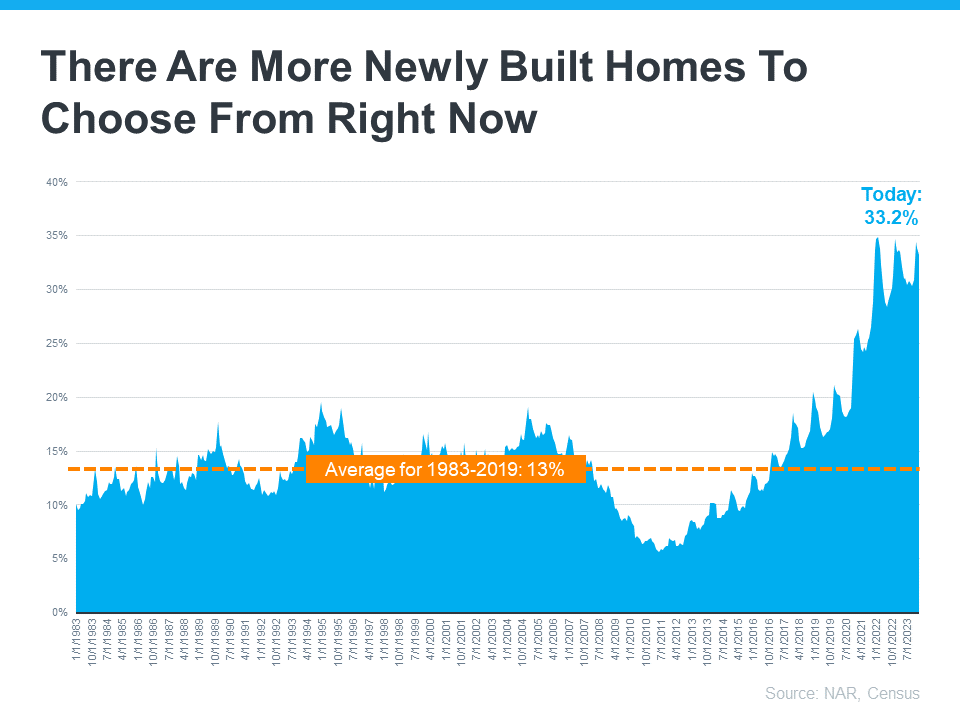

Data from the Census and the National Association of Realtors (NAR) shows that newly built homes are a bigger part of today’s housing inventory than the norm (see graph below):

From 1983 to 2019 (the last normal year in the market), newly built homes made up only 13% of the total inventory of homes for sale. But today that number has climbed to over 33%.

Rest assured, after over a decade of underbuilding, builders aren’t overdoing it today. Even with an increase in new construction today, there’s still a significant housing shortage overall. But for you, the uptick in new builds can be a game changer because it gives you more options for your search.

2. Newly Built Homes May Be More Affordable Than You’d Think

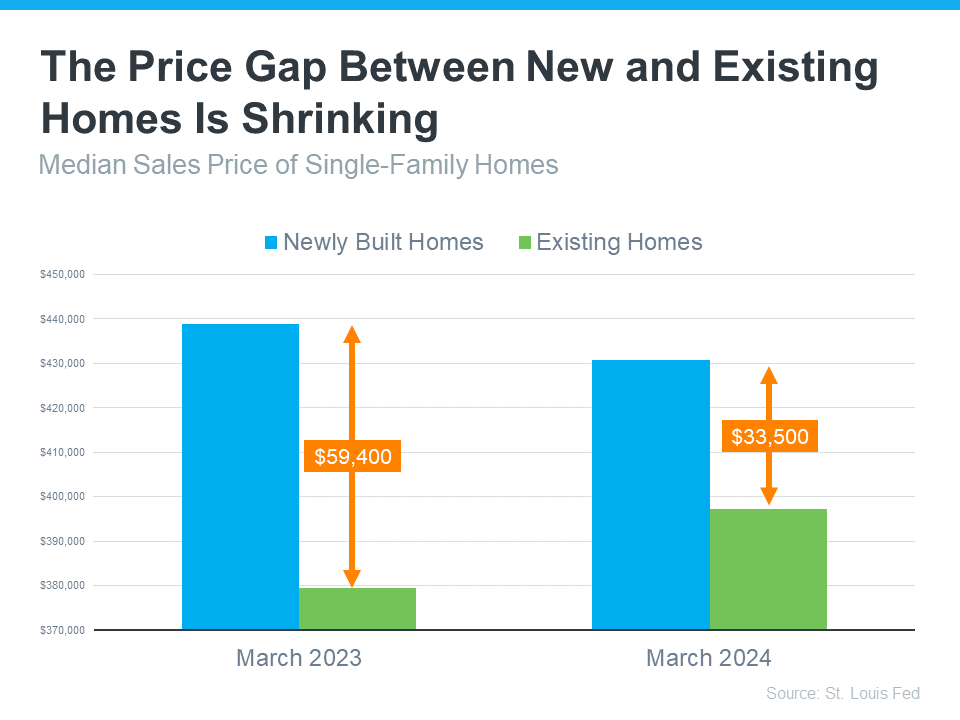

You may still be wondering if a new build could really be an option for you. If you’ve previously written them off because you thought they would be out of your budget, consider this. The price gap between a newly built home and an existing house is shrinking. Here's why.

Builders are going to build what’s in demand. And they know people need more options right now, especially ones that are smaller and potentially more affordable. So, they’re focusing on building smaller homes at lower price points. The graph below shows the price difference between new and existing homes is shrinking as that happens:

As LendingTree explains:

“In the past, newly built homes have been much more expensive than existing homes — but that gap has been getting smaller recently. In some places today, you may find that the cost to build versus buy is roughly the same.”

And an article from CNBC says:

“While new builds are still sold for slightly more than existing homes, the price gap has significantly narrowed . . .”

Not to mention, some builders are even offering price cuts and mortgage rate buy-downs right now to sweeten the deal. Today there are many reasons new builds may be worth considering. Other buyers sure seem to think so. As Freddie Mac says:

"As the supply of existing homes for sale remains low and home prices continue to rise, more buyers are choosing to purchase new homes than in previous years."

Just know that buying a newly built home isn’t the same as buying an existing one. Builder contracts have different fine print. So, partner with a local agent who knows the market, builder reputations, and what to look for in those contracts so you have an expert on your side to help you explore this option.

Bottom Line

If you want to find out what builders are doing in our area, let’s connect and check it out together. And if you’re willing to cast a wider net to open up your options even more, we can talk about broadening your search to include other towns nearby.

Tips for Younger Homebuyers: How To Make Your Dream a Reality

If you’re a member of a younger generation, like Gen Z, you may be asking the question: will I ever be able to buy a home? And chances are, you’re worried that’s not going to be in the cards with inflation, rising home prices, mortgage rates, and more seemingly stacked against you.

While there’s no arguing this housing market is challenging for first-time homebuyers, it is still achievable, especially if you have professionals on your side.

Here are some helpful tips you may get from a pro.

1. Explore Your Options for a Down Payment

If a down payment is your #1 hurdle, you may have options to give your savings a boost. There are over 2,000 down payment assistance programs designed to make homeownership more achievable. And, that’s not the only place you may be able to get a helping hand. While it may not be an option for everyone, 49% of Gen Z homebuyers got money from loved ones that they used toward a down payment, according to LendingTree.

And chances are you won’t need to put 20% down (unless specified by your loan type or lender). So be sure to work with a trusted mortgage professional to explore your options, find out how much you’ll really need, and learn about any guidelines on getting a gift from loved ones.

2. Live with Loved Ones To Boost Your Savings

Another thing a number of Gen Z buyers are doing is ditching their rental and moving back in with friends or family. This can help cut down your housing costs so you can build your savings a whole lot faster. As Bankrate explains:

“. . . many have opted to stop renting and live with family in order to boost their savings. Thirty percent of Gen Z homebuyers move directly from their family member’s home to a home of their own, according to NAR.”

3. Cast a Broad Net for Your Search

When you’ve saved up enough, here’s how a pro will help you approach your search. Since the supply of homes for sale is still low and affordability is tight, they’ll give you strategies and avenues you may not have considered to open up your pool of options.

For example, it’s usually more affordable if you consider a rural or suburban area versus an urban one. So, while the city may be livelier and more energetic, the cost of living may be reason enough to look at something further out. And if you consider smaller homes and condos or townhouses, you’ll give yourself even more ways to break into the market. As Colby Stout, Research Analyst at Bright MLS, explains:

“Being flexible on the types of home (e.g., a condo or townhome versus a single-family home) and exploring more affordable neighborhoods is important for first-time buyers.”

4. Take a Close Look at Your Wants and Needs

And lastly, an agent can help you really think about your must-have’s and nice-to-have’s. Remember, your first home doesn’t have to be your forever home. You just need to get your foot in the door to start building equity. If you want to buy, you may find making some compromises is worth it. As Chase says:

“An open-minded approach to house-hunting may be one way for Gen Z homebuyers to maintain some edge. This could mean buying in areas that are less expensive. Differentiating needs vs. wants may help in this area as well.”

An agent will help you prioritize your list of home features and find houses that can deliver on the top ones. And they’ll be able to explain how equity can benefit you in the long run and make it possible to move into that dream home down the line.

Bottom Line

Real estate professionals have expertise on what’s working for other buyers like you. Lean on them for tips and advice along the way. As Directors Mortgage says, with that support you can make it happen:

“The path to homeownership may not be a straightforward one for Gen Z, but it’s undoubtedly within reach. By adopting the right strategies, like exploring down payment assistance programs and sharing living costs with relatives, you can bring your dream of owning a home closer to reality.”

Let’s connect to get you set up for long-term success.

What Is Going on with Mortgage Rates?

You may have heard mortgage rates are going to stay a bit higher for longer than originally expected. And if you’re wondering why, the answer lies in the latest economic data. Here’s a quick overview of what’s happening with mortgage rates and what experts say is ahead.

Economic Factors That Impact Mortgage Rates

When it comes to mortgage rates, things like the job market, the pace of inflation, consumer spending, geopolitical uncertainty, and more all have an impact. Another factor at play is the Federal Reserve (the Fed) and its decisions on monetary policy. And that’s what you may be hearing a lot about right now. Here’s why.

The Fed decided to start raising the Federal Funds Rate to try to slow down the economy (and inflation) in early 2022. That rate impacts how much it costs banks to borrow money from each other. It doesn't determine mortgage rates, but mortgage rates do respond when this happens. And that’s when mortgage rates started to really climb.

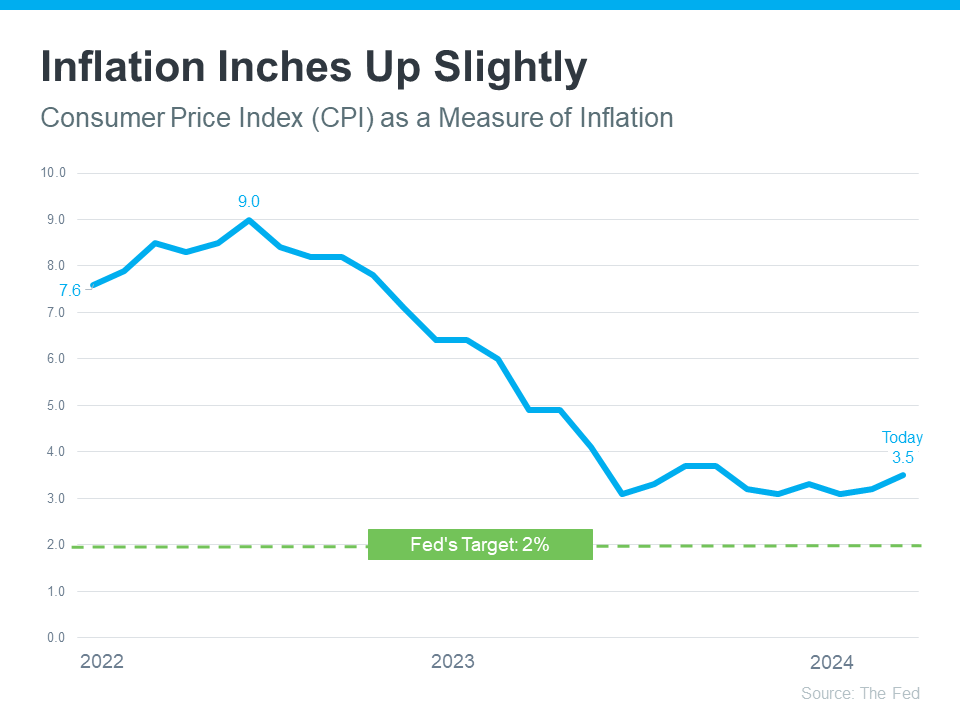

And while there’s been a ton of headway seeing inflation come down since then, it still isn’t back to where the Fed wants it to be (2%). The graph below shows inflation since the spike in early 2022, and where we are now compared to their target rate:

As the graph shows, we’re much closer to their goal of 2% inflation than we were in 2022 – but we’re not there yet. It's even inched up a hair over the last 3 months – and that’s having an impact on the Fed’s plans. As Sam Khater, Chief Economist at Freddie Mac, explains:

“Strong incoming economic and inflation data has caused the market to re-evaluate the path of monetary policy, leading to higher mortgage rates.”

Basically, long story short, inflation and its impact on the broader economy are going to be key moving forward. As Greg McBride, Chief Financial Analyst at Bankrate, says:

“It’s the longer-term outlook for economic growth and inflation that have the greatest bearing on the level and direction of mortgage rates. Inflation, inflation, inflation — that’s really the hub on the wheel.”

When Will Mortgage Rates Come Down?

Based on current market data, experts think inflation will be more under control and we still may see the Fed lower the Federal Funds Rate this year. It’ll just be later than originally expected. As Mike Fratantoni, Chief Economist at the Mortgage Bankers Association (MBA), said in response to the Federal Open Market Committee (FOMC) decision yesterday:

“The FOMC did not change the federal funds target at its May meeting, as incoming data regarding the strength of the economy and stubbornly high inflation have resulted in a shift in the timing of a first rate cut. We expect mortgage rates to drop later this year, but not as far or as fast as we previously had predicted.”

In the simplest sense, what this says is that mortgage rates should still come down later this year. But timing can shift as new employment and economic data come in, geopolitical uncertainty remains, and more. This is one of the reasons it’s usually not a good strategy to try to time the market. An article in Bankrate gives buyers this advice:

“ . . . trying to time the market is generally a bad idea. If buying a house is the right move for you now, don’t stress about trends or economic outlooks.”

Bottom Line

If you have questions about what’s happening in the housing market and what that means for you, let’s connect.

The Perks of Buying over Renting

Thinking about buying a home? While today’s mortgage rates might seem a bit intimidating, here are two solid reasons why, if you’re ready and able, it could still be a smart move to get your own place.

1. Home Values Typically Go Up Over Time

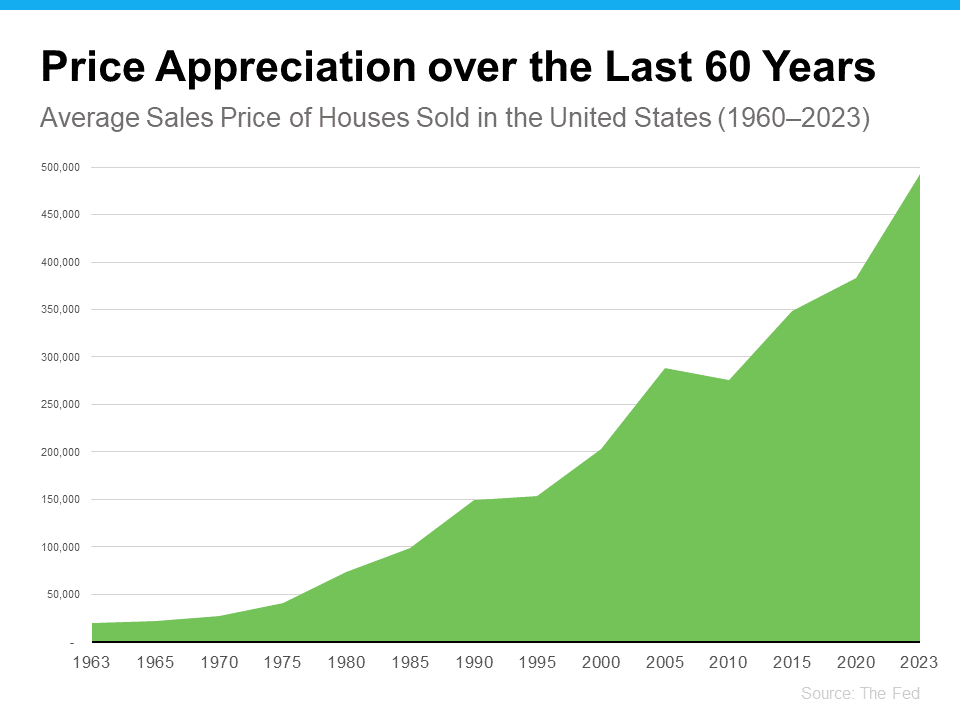

There’s been some confusion over the past year or so about which way home prices are headed. Make no mistake, nationally they’re still going up. In fact, over the long-term, home prices almost always go up (see graph below):

Using data from the Federal Reserve (the Fed), you can see the overall trend is home prices have climbed steadily for the past 60 years. There was an exception during the 2008 housing crash when prices didn't follow the normal pattern, but generally, home values kept rising.

This is a big reason why buying a home can be better than renting. As prices go up and you pay down your mortgage, you build equity. Over time, this growing equity can really increase your net worth. The Urban Institute says:

“Homeownership is critical for wealth building and financial stability.”

2. Rent Keeps Rising in the Long Run

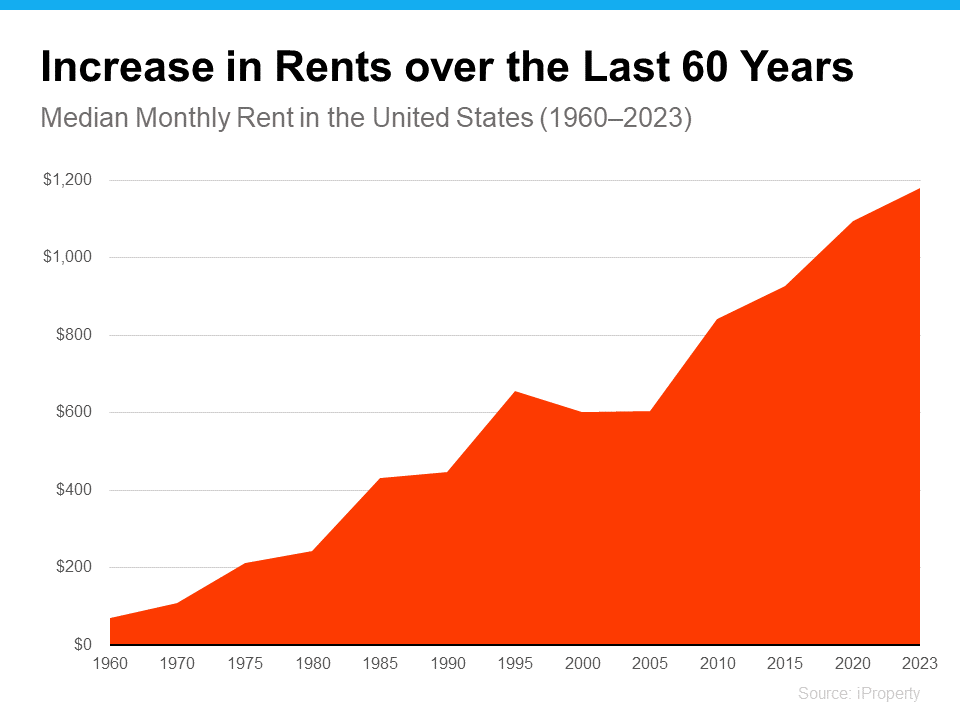

Here’s another reason you may want to think about buying a home instead of renting – rent just keeps going up over the years. Sure, it might be cheaper to rent right now in some areas, but every time you renew your lease or sign a new one, you’re likely to feel the squeeze of your rent getting higher. According to data from iProperty Management, rent has been going up pretty consistently for the last 60 years, too (see graph below):

So how do you escape the cycle of rising rents? Buying a home with a fixed-rate mortgage helps you stabilize your housing costs and say goodbye to those annoying rent increases. That kind of stability is a big deal.

Your housing payments are like an investment, and you've got a decision to make. Do you want to invest in yourself or keep paying your landlord?

When you own your home, you're investing in your own future. And even when renting is cheaper, that money you pay every month is gone for good.

As Dr. Jessica Lautz, Deputy Chief Economist and VP of Research at the National Association of Realtors (NAR), says:

“If a homebuyer is financially stable, able to manage monthly mortgage costs and can handle the associated household maintenance expenses, then it makes sense to purchase a home.”

Bottom Line

If you're tired of your rent going up and want to explore the many benefits of homeownership, let’s talk to explore your options.

|

Press Ctrl + D to bookmark this page

Web Accessibility Help Visually Impaired

Physical Difficulty

Audio Impaired

|

Member Agents | Privacy Policy

Realtor Websites by TourRE